Getting into debt is easy, but getting out can be hard work.

Nonetheless, the debt snowball method can help you work your way to debt freedom quickly and strategically.

Using this method, you pay off debt progressively from the smallest balance to the largest balance.

Each time you pay off a debt, you roll the money that would be used for that debt to pay off the next smallest debt.

As you pay off each debt, you’ll have more money available to apply to the next smallest debt. This progressive growth of available funds mimics a snowball getting larger as it rolls down a hill. Hence the name “debt snowball.”

Why the Debt Snowball Method Works

The debt snowball method leverages momentum over math.

The idea is to get a quick win by paying off a small debt first. This win will give you the motivation to continue aggressively attacking your debt.

It’s the same psychology that’s necessary for weight loss. If you can lose those first few pounds quickly, you’ll be motivated to continue your regimen and lose more weight.

This approach is what distinguishes it from the debt avalanche method.

What is the debt avalanche method?

The debt avalanche method is intended to save you the most money overall by attacking your debt from the highest interest rate to the smallest.

Though, both methods will get you to the ultimate goal of paying off debt.

How to Use the Debt Snowball

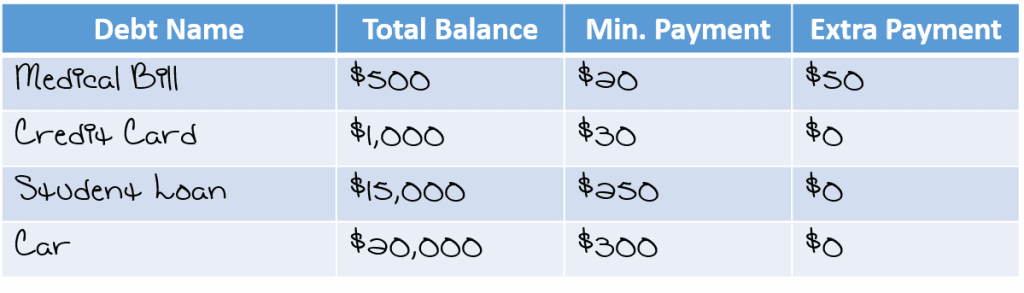

Using the debt snowball method is quite simple, as it only consists of four steps. In the example below, I’ll show you how the debt snowball works.

Step 1: List all of your debt from smallest to largest

If you’re following Dave Ramsey’s baby steps, then you’ll exclude the mortgage from your snowball since it’ll be paid off at a later time.

Step 2: Pay the minimum on all debts except the smallest

For this step, you’ll need to take a look at your budget and find ways to cut your expenses. You may also need to pick up a side hustle and put any extra money that you make toward paying off the smallest debt.

Step 3: Pay off the smallest debt then apply the money from that debt to your next smallest balance

As you continue to put extra money toward your debt, you’ll find that you’ll pay it off quickly.

Once the smallest debt is paid off, roll the money that was going toward it to pay off the next smallest debt.

This will include the minimum payment and any extra payments that you were making toward the debt.

Step 4: Repeat until all debts are paid off

Continue this method until all debts are paid off and you’re debt free!

Debt snowball spreadsheet

If you’re looking for a debt snowball spreadsheet, I’ve actually created one that can help you track your debt payoff!

This spreadsheet includes:

- Debt snowball worksheet & debt payoff tracker to help you get out of debt fast!

- Monthly & paycheck budget templates – you decide which works best for you!

- Budget examples with real numbers that you can use as a guide (examples ALWAYS help!)

- A bill payment tracker to keep track of when bills need to be paid

- An expense tracker to keep track of your spending

- Savings goal/emergency fund trackers that’ll keep you motivated to reach your goals

- Video instructions on how to use your binder (because sometimes you just need extra help!)

You can also grab these my debt snowball printable if you’d prefer to write out your debt snowball.

Using the debt snowball to pay off student loans

The debt snowball is a great method for paying off debt. It makes paying off your debt seem a lot more attainable when you’re able to tackle your small debt first.

In fact, it’s exactly what I used to pay off over $78,000 in student loan debt in less than three years.

Of course, there are many other methods that you can try. So choose what works best for you and your financial situation.